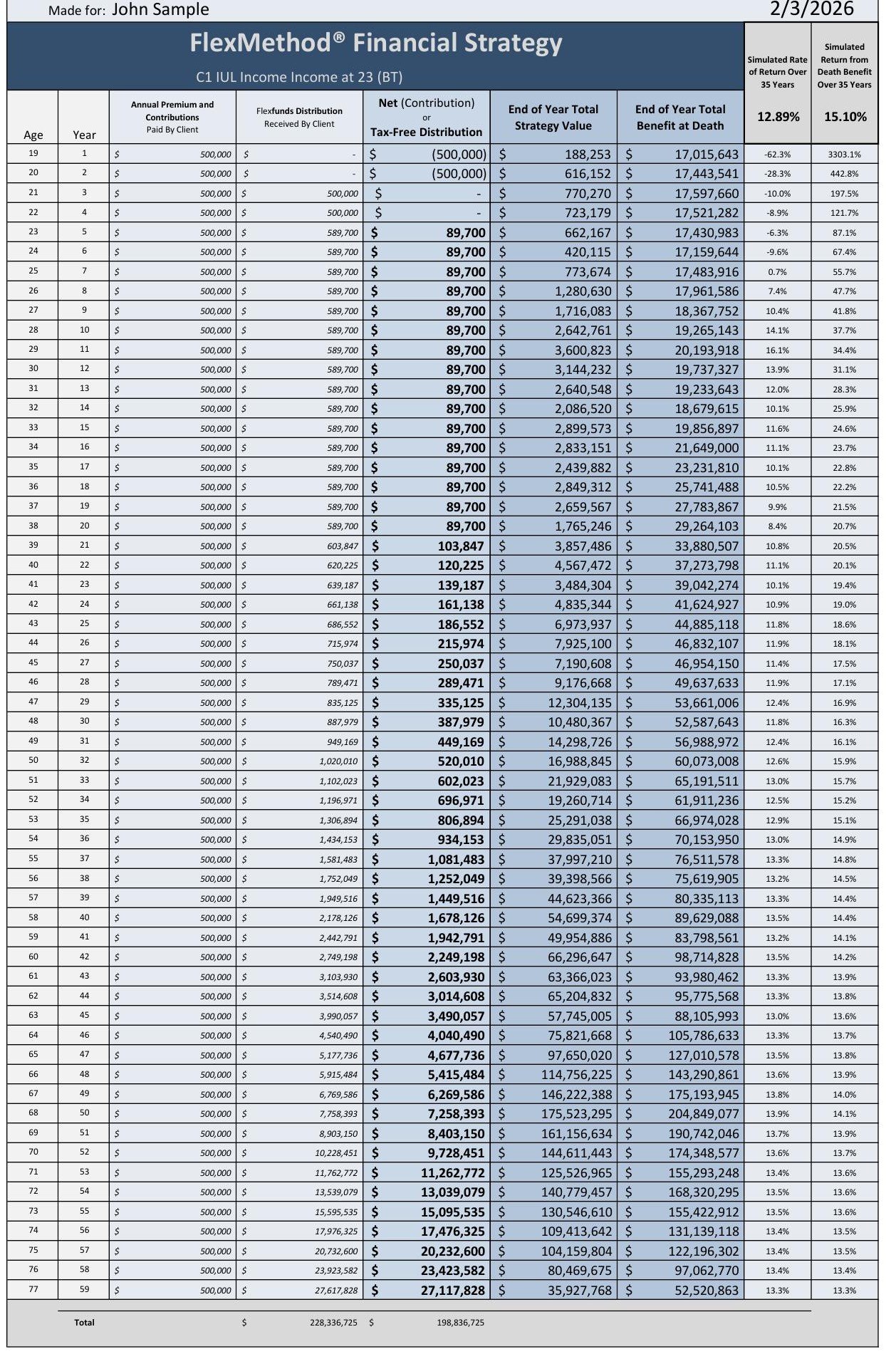

By reviewing this design, you acknowledge and agree to the following:

1.Conceptual Numbers – All values used in this design are conceptual and are not guaranteed by any party, including your agent, wealth consultant, any life insurance carrier, or US Life. These values are for illustrative purposes only.

2.Non-Carrier Illustrated Figures – The figures presented in this design are not carrier-illustrated numbers. The Flexmethod is not an insurance product itself; rather, it incorporates insurance products into your overall financial strategy.

3. Refer to Carrier Illustration – Before moving forward, you will be provided with a copy of the official policy illustration from the carrier. The carrier’s illustration will contain the detailed terms and conditions of your policy and should be referred to for accurate information regarding your policy.4.Indexed Universal Life Policy (IUL) Performance – If you are using an Indexed Universal Life (IUL) policy, its performance will be based on the returns from external indexes. This design simulates potential index performance but does not represent actual future returns. Actual returns may be more or less favorable than the assumptions used in this design.

5.Borrowing Risks – Borrowing from an insurance policy introduces additional risks, including the possibility of the policy lapsing if the amount borrowed exceeds the surrender value. Borrowing may also affect or eliminate any guarantees provided by the insurance carrier. If your policy lapses, you will lose the death benefit and may incur tax liabilities on the borrowed amounts.

6. Interest Rate Assumptions – The borrowing rates used in this illustration are assumed for simulation purposes and may differ from actual future rates. These rates are not guaranteed and will fluctuate over time. The actual borrowing rates could be more or less favorable than those shown in this design.

7. Core Assumption – The Flexmethod strategy is based on the assumption that, on average, the cost of borrowing from the insurance policy will be lower than the average returns earned by the policy. While we believe our assumptions are conservative, there is a possibility that actual outcomes may differ, and this assumption may not hold true.

8.Not Tax Advice – Any references to taxes in this design should not be interpreted as tax advice. US Life and its wealth consultants are not licensed tax advisors. You should consult your own tax professional regarding the potential tax implications of the Flexmethod strategy as it relates to your specific situation.